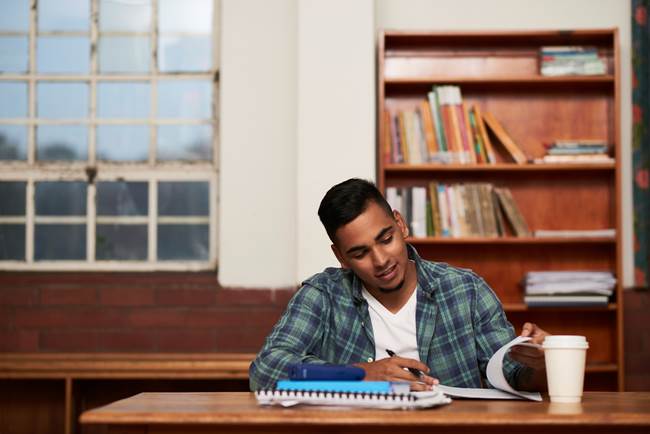

Few South Africans have the financial means to self-fund a tertiary education, start a business, renovate a home, buy a car, or cover other large up-front expenses.

Household savings in South Africa are notably low and, according to data from the South African Reserve Bank (SARB) and the Organisation for Economic Cooperation and Development (OECD), most South Africans tend to consume most or all of their income.

For people wanting to improve their circumstances or respond to unexpected events, personal loans can be a helpful financial tool – if used wisely .

The application process is quick and straightforward, with fast approval times.

Because personal loans are unsecured, borrowers don’t need to provide security. Once the loan is approved, the funds are transferred directly into the applicant’s account.

“Credit isn’t inherently bad, and can be a catalyst for achieving your goals. But responsible borrowing is critical. This means only borrowing what you can afford, planning for repayments, and using credit carefully, not for short-term gratification,” says Gavyn Letley, Product Head at DirectAxis.

He suggests considering the following before applying for credit:

- Borrow for the right reasons: Funding further education to improve career prospects, buying an income-generating asset such as a mobile coffee bar, or starting a small business are examples of constructive credit use.

- Have a plan: Before taking on any debt, draw up a budget listing your income and expenses. You will then be able to calculate the repayments you can reasonably afford to make. A good rule of thumb is that your total debt repayments should not exceed 30% of your income. You can use a loan repayment calculator, such as www.directaxis.co.za/loans/personal-loan/calculator, to work out the repayments for the loan, interest and fees.

- Understand the terms: Read the contract and understand the terms of the loan. Know the interest rate and total cost of credit, including any administration fees, and what the repayment schedule is before you agree. Check whether the agreement includes credit life insurance and what it covers. This is insurance that covers your debt repayments if you are unable to pay due to life events such as temporary or permanent disability, involuntary unemployment, retrenchment and, in some cases, critical illness.

- Keep a clean credit history: Pay on time and avoid skipping payments. This will ensure you retain a good credit score. A good score will enable you to access more financial products at better interest rates. There are plenty of free tools you can use to check your credit score, including Pulse, a financial-wellness tool that allows you to check your credit rating and how to improve it.

“When used constructively, credit can provide access to opportunities that may otherwise be out of reach. Whether it’s pursuing a degree or diploma, launching a start-up or covering the relocation costs for a new job, credit can be a stepping stone rather than a stumbling block,” says Letley.

Gwen Bosman

Soweto Sunrise News

{kind=link}